SMR Investment Surge: Why Smart Money Is Backing Small Modular Reactors

The Return of Nuclear in the Net-Zero Era

Nuclear energy is no longer the energy of the past—it’s rapidly becoming the power source of the future. As the world races to meet net-zero carbon goals, traditional renewables like wind and solar face limitations in reliability and scalability. Enter Small Modular Reactors (SMRs)—a new generation of compact, factory-built nuclear power systems that promise to deliver clean, continuous, and decentralized electricity. With energy demand surging from AI, electric vehicles, and industrial digitization, SMRs are attracting attention as a crucial piece of the next-gen energy puzzle.

Governments, venture capitalists, and tech giants are now investing billions into SMR technologies, recognizing their potential to provide carbon-free baseload power where large reactors can’t go. From the U.S. Department of Energy’s strategic subsidies to Microsoft’s power deal with Oklo, the momentum behind SMRs is real. Even legacy energy giants and advanced manufacturing firms are entering the race, betting that modular nuclear will play a central role in decarbonizing power-hungry sectors.

In this blog, we’ll unpack the technologies behind this nuclear resurgence, examine where the capital is flowing—from governments to tech giants—and spotlight the leading players shaping the SMR landscape. You’ll gain insights into how SMRs are being deployed across sectors, why investors are treating them as strategic infrastructure, and what this means for the future of clean energy, digital growth, and grid resilience.

How SMRs Are Reshaping Nuclear Energy

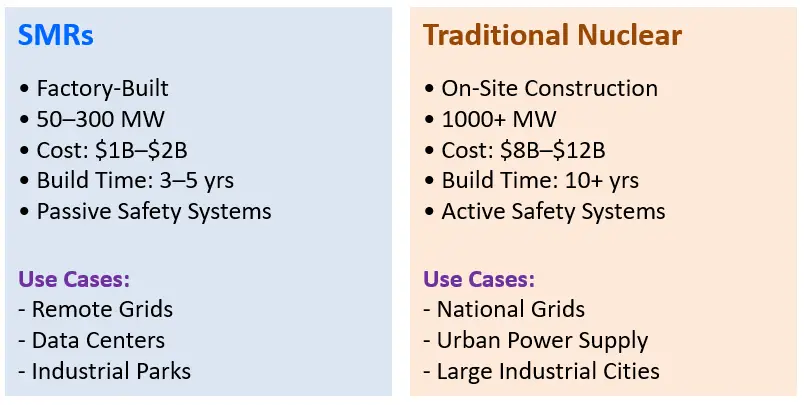

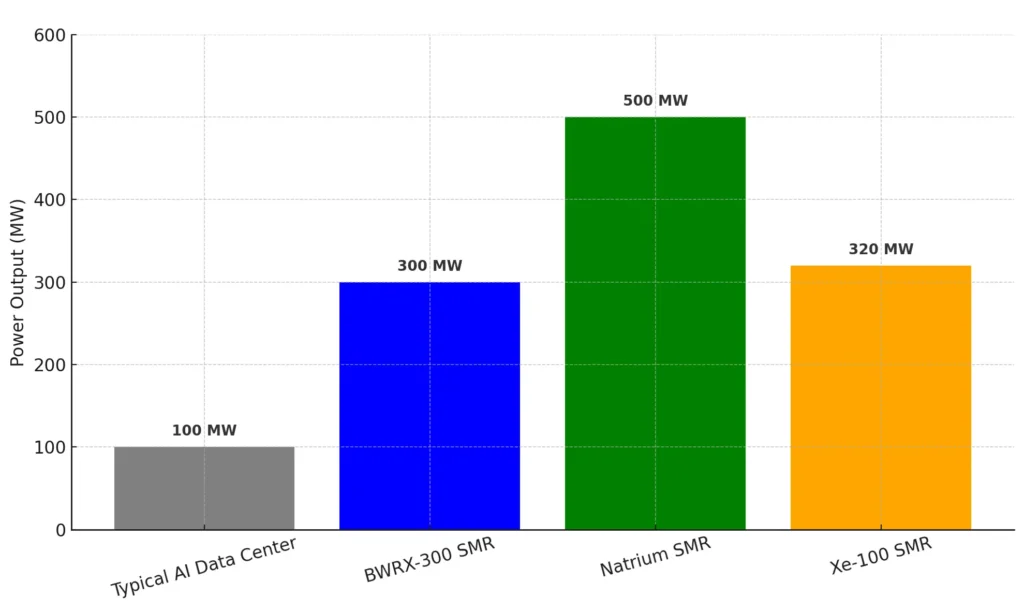

Small Modular Reactors, or SMRs, represent a transformative step in the evolution of nuclear energy. Unlike traditional nuclear plants, which require massive construction sites, multibillion-dollar budgets, and a decade or more to build, SMRs are compact, factory-manufactured units designed for scalability and speed. These reactors typically generate 50 to 300 megawatts of electricity—ideal for powering data centers, industrial parks, and isolated regions where large nuclear facilities aren’t practical.

One of the biggest advantages of SMRs is their standardized, modular construction. Core components are assembled in controlled factory settings and transported to sites for installation, dramatically reducing construction risk, permitting delays, and overall project cost. Many designs incorporate passive safety systems that operate without external power or human intervention—addressing long-standing public concerns about nuclear safety.

Unlike intermittent renewables like wind and solar, SMRs provide reliable baseload power with a small physical footprint and zero carbon emissions. This makes them especially valuable in high-demand, high-stability environments such as data infrastructure, military bases, and clean hydrogen production. The image below highlights how SMRs compare to traditional nuclear power plants in terms of size, cost, build time, and use cases:

Figure: SMRs offer a scalable, lower-cost, and safer alternative to traditional gigawatt-scale nuclear plants.

The Global Investment Landscape in SMRs (2024–2030)

As the global clean energy race intensifies, Small Modular Reactors (SMRs) are attracting unprecedented levels of investment from both governments and private industry. Once considered a futuristic alternative to conventional nuclear, SMRs are now being recognized as critical infrastructure for achieving net-zero goals, stabilizing grids, and powering energy-intensive technologies like AI and hydrogen.

🌍 Government Initiatives Driving the Shift

Several national governments have made bold financial commitments to advance SMR deployment. In the United States, the Department of Energy has committed over $1.4 billion to fast-track reactors from companies like TerraPower, X-Energy, and Oklo. The United Kingdom has pledged £385 million to Rolls-Royce’s SMR program with a vision to deploy 16 units by the 2030s. Canada is moving faster than most, with the Darlington BWRX-300 SMR project targeting full deployment by 2028. Meanwhile, South Korea, France, Poland, and China have integrated SMRs into their long-term energy strategies.

🏦 Private Capital Accelerates Commercialization

On the private side, investment momentum is growing. Bill Gates’ TerraPower is leading a $4B funding effort for the Natrium reactor in Wyoming. Microsoft has signed a power purchase agreement with Oklo to supply carbon-free energy to future AI infrastructure. Other players like GE Hitachi, Holtec, and X-Energy are forming global partnerships and attracting institutional funding, signaling growing market confidence.

Top SMR Technologies Nearing Commercial Deployment

Not all SMRs are created equal. While the overall concept centers around compact, modular nuclear designs, the technological diversity within the SMR field is vast. Different cooling systems, fuel types, and output capacities are being tested globally, and only a few have reached commercial readiness by 2030.

⚙️ GE Hitachi – BWRX-300

The BWRX-300 is widely considered the frontrunner. Backed by GE Hitachi and Ontario Power Generation, this boiling water reactor design uses established light-water technology and has already entered the pre-construction phase at Darlington, Canada, with a deployment target of 2028. Its regulatory simplicity and low cost-per-megawatt make it a top choice for utilities in Canada, Poland, and the U.S.

⚛️ Rolls-Royce SMR (UK)

With strong UK government support and industrial backing, Rolls-Royce’s SMR is a pressurized water reactor producing 470 MWe—larger than most peers. Its modular factory-based assembly aims to deliver units faster and cheaper than traditional nuclear. Deployment is expected by the early 2030s, with licensing already in progress.

🔥 TerraPower – Natrium

Funded by Bill Gates and partnered with Bechtel, the Natrium reactor uses sodium cooling and includes molten salt energy storage, allowing for flexible output (up to 500 MWe during peak demand). The first site in Wyoming is under development with an expected deployment by 2030, contingent on HALEU fuel supply.

☢️ X-Energy – Xe-100

This helium-cooled, high-temperature gas reactor uses TRISO fuel for enhanced safety and is ideal for industrial heat applications like hydrogen and chemical production. With backing from Dow Chemical and the U.S. DOE, its first deployment is planned for the Texas Gulf Coast by 2030.

🧪 NuScale – VOYGR

Though once a leader, NuScale’s VOYGR platform has seen delays after the cancellation of its Utah project. Despite this, it remains the only SMR design certified by the U.S. NRC, and the company continues to pursue deployments in Romania, Poland, and Ukraine.

🌐 Other Notable Emerging Designs

🇰🇷 SMART (South Korea – UAE Partnership)

Developed by KAERI, the SMART SMR is a 100 MWe pressurized water reactor designed for export and flexible siting. It was licensed in Korea in 2012 and is being jointly explored with the UAE under ENEC. While not yet deployed, it represents one of the most mature government-developed SMR designs outside the West.

🇺🇸 Oklo Aurora

A 1.5 MWe microreactor targeting data centers and off-grid facilities. It’s backed by Microsoft and in regulatory review.

🇩🇰 Seaborg CMSR

A barge-mounted molten salt reactor, designed in Denmark, targeting Southeast Asian markets with deployment potential by 2028.

Why Big Tech Is Betting on SMRs

While governments have taken the lead in early SMR deployment, Big Tech is quietly moving in—and not just out of curiosity. The convergence of AI, cloud, and quantum computing is pushing energy demand to extremes, forcing companies like Microsoft, Amazon, and Google to explore stable, scalable, and carbon-free power sources. SMRs offer a compelling answer.

🧠 AI and Data Centers Are Pushing the Grid to Its Limits

The rise of AI workloads and hyperscale computing has turned data centers into energy-intensive infrastructure. Some training runs for large language models consume more than 1 GWh—equivalent to what 100 U.S. homes use in a year. A single cloud campus can demand 50–500 MW, often requiring new substations or direct grid interconnection. With many renewable sources still intermittent, Big Tech is seeking alternatives that align with climate pledges without compromising reliability.

⚡ SMRs as On-Site, Carbon-Free Power

Unlike solar or wind, SMRs provide round-the-clock baseload power from a compact footprint. They can be co-located with data centers, reducing transmission losses and bypassing overburdened regional grids. Microsoft has already signed a power purchase agreement (PPA) with Oklo, a microreactor startup, aiming to use SMRs for powering AI infrastructure. TerraPower and Bechtel are also positioning their Natrium reactor as a solution for clean industrial loads, including compute clusters.

For tech giants balancing performance, carbon neutrality, and geographic flexibility, SMRs are emerging not just as energy sources—but as infrastructure enablers for the next wave of digital growth.

For tech giants balancing performance, carbon neutrality, and geographic flexibility, SMRs are emerging not just as energy sources—but as infrastructure enablers for the next wave of digital growth. The infographic below compares the energy demands of a typical AI data center with the output capacities of leading SMR technologies—illustrating why these compact reactors are attracting serious attention from the cloud and AI sectors.

Strategic Use Cases: Beyond Electricity

Small Modular Reactors are not just about electricity—they are about multi-role infrastructure. SMRs offer unique thermal and spatial characteristics that make them versatile in industrial, environmental, and even defense contexts. As the world moves beyond electrification into sectors like hydrogen, desalination, and space, SMRs are quietly positioning themselves at the heart of future systems.

🔋 Industrial Heat and Hydrogen Production

Many SMR designs—especially high-temperature gas-cooled reactors like Xe-100—can produce process heat above 750°C, making them ideal for hard-to-decarbonize industries such as cement, ammonia, steel, and hydrogen electrolysis. SMRs can power electrolysis directly or provide steam for thermochemical hydrogen production, enabling low-carbon hydrogen at scale.

🌊 Desalination and Water Infrastructure

In arid and coastal regions, SMRs can serve dual purposes: electricity generation and thermal desalination. Countries like Saudi Arabia and China are exploring SMR-powered desalination as a long-term solution to water scarcity—especially in off-grid or low-infrastructure zones.

🛰️ Defense, Space, and Remote Sites

SMRs are particularly suited for military bases, islands, and off-grid installations. The U.S. Department of Defense is actively developing microreactors for forward bases (e.g., Project Pele). In space, NASA and DOE are evaluating nuclear thermal propulsion and lunar power modules based on SMR principles.

Key Market Enablers and Barriers

Despite rising interest and billions in committed capital, the path to full-scale SMR deployment is far from guaranteed. Investors, developers, and policymakers must navigate a complex landscape of technical, regulatory, and societal factors. Understanding what’s accelerating SMRs—and what could slow them down—is critical for assessing risk and opportunity.

✅ Market Enablers

Several key factors are working in favor of SMRs. First, the global policy shift toward firm clean energy has positioned modular nuclear as an essential complement to wind and solar. Second, standardization and factory fabrication reduce construction risk and capex volatility—two chronic issues in traditional nuclear. Third, emerging applications in AI, hydrogen, and defense are creating new, high-value demand verticals.

Financial incentives are also growing. In the U.S., the Inflation Reduction Act (IRA) extends tax credits to advanced nuclear. The EU’s Net Zero Industry Act includes SMRs in its strategic cleantech scope. Regulatory bodies in Canada, the UK, and the U.S. have begun streamlining licensing pathways for approved designs.

⚠️ Market Barriers

Yet challenges remain. Public opposition to anything labeled “nuclear” still runs deep in many regions. The supply chain for HALEU fuel, needed for several advanced designs like Natrium and Xe-100, is currently fragile and concentrated in geopolitically sensitive regions. Moreover, the lack of real-world performance data for most SMRs may delay adoption by conservative utilities and investors seeking proven returns.

SMR vs. Renewables: Investment Comparison

As capital pours into decarbonization technologies, investors face a core question: Where does nuclear—particularly SMRs—fit within the clean energy portfolio? While renewables like wind and solar dominate headlines, SMRs are building a strong case not as competitors, but as complementary assets with distinct financial and operational roles.

💵 Cost and Output Profile

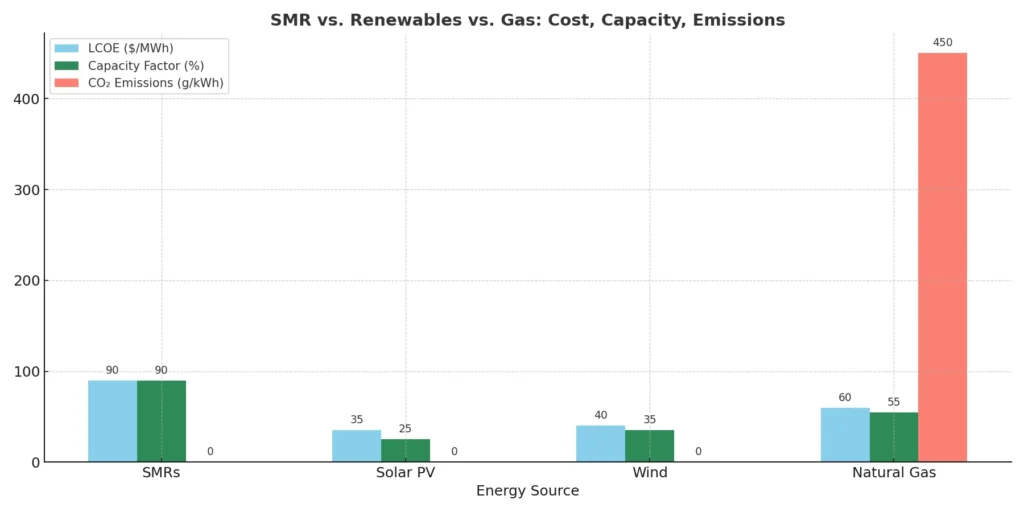

SMRs have higher upfront capital costs than solar or wind, often between $1.5 to $3 million per MW. However, they offer round-the-clock baseload power with minimal land use and no need for battery storage. Their capacity factors often exceed 90%, far above wind (~35%) or solar (~25%). This means fewer fluctuations in revenue streams and greater reliability for industrial loads or AI infrastructure.

📊 Risk and ROI Outlook

Renewables typically win on speed-to-market and scale, but are vulnerable to intermittency and long-term grid saturation. SMRs, while slower to deploy, offer a longer asset life, stable cash flow, and high capacity utilization. For investors seeking exposure to clean firm power, especially in regions with growing data demand or weak grids, SMRs are emerging as a high-upside, policy-backed frontier.

The chart below compares SMRs with renewables and gas across cost, capacity, and carbon dimensions.

The Future Outlook: Timeline to Commercial Viability

While Small Modular Reactors have moved from concept to construction, the next decade will determine whether they become mainstream infrastructure or remain a niche technology. Several leading designs are already in advanced stages of development—with firm deployment timelines, government backing, and active licensing tracks.

By 2028, the first commercial SMR—GE Hitachi’s BWRX-300—is expected to go online in Darlington, Canada. The Natrium reactor (TerraPower) and Xe-100 (X-Energy) aim for U.S. deployment by 2030, while Rolls-Royce’s UK SMR is targeting early 2030s rollouts across the UK. Simultaneously, China’s Linglong One could become the world’s first fully operational SMR, potentially entering service before 2027.

Globally, over 70 SMR designs are under development across 18+ countries. As licensing frameworks mature, and as public-private partnerships deepen, analysts expect select SMRs to reach wide-scale commercial adoption by 2035—particularly in markets with unstable grids, heavy industry, or high carbon reduction mandates.

Final Thoughts: Is Now the Time to Invest in SMRs?

Small Modular Reactors are no longer theoretical—they’re moving into the real world with momentum, capital, and policy support behind them. From data centers to hydrogen hubs, from military bases to industrial zones, SMRs are positioned to fill a critical gap in the global energy mix: clean, firm, and scalable power.

For investors, the next five years offer a rare opportunity to gain exposure before SMRs reach mainstream adoption. The players, the technologies, and the policy frameworks are aligning. The only question left is: Are you positioned for the nuclear comeback?

📚 References

- U.S. Department of Energy (2024) – Advanced Reactor Demonstration Program (ARDP)

https://www.energy.gov/ne/nuclear-reactor-technologies/advanced-reactor-demonstration-program - Ontario Power Generation (2024) – Darlington New Nuclear Project (BWRX-300)

https://www.opg.com/projects/clean-energy/darlington-new-nuclear/ - Rolls-Royce SMR Ltd. (2024) – Official SMR Program Overview

https://www.rolls-royce-smr.com/ - TerraPower (2024) – Natrium Reactor Overview

https://www.terrapower.com/our-work/natrium-reactor/ - X-Energy (2024) – Xe-100 Advanced High-Temperature Gas Reactor

https://x-energy.com/reactors/xe100 - NuScale Power (2024) – VOYGR SMR Systems

https://www.nuscalepower.com/projects/voygr-smr-plants - Lazard (2023) – Levelized Cost of Energy Analysis – Version 15.0

https://www.lazard.com/perspective/levelized-cost-of-energy-levelized-cost-of-storage-and-levelized-cost-of-hydrogen/ - International Energy Agency (IEA) (2023) – Advanced Nuclear Power: Status and Outlook

https://www.iea.org/reports/advanced-nuclear-power - Oklo Inc. (2023) – Microsoft Signs Power Purchase Agreement with Oklo

https://www.oklo.com/news/microsoft-oklo-ppa-announcement - International Atomic Energy Agency (IAEA) (2024) – Small Modular Reactors Technology Developments

https://www.iaea.org/topics/small-modular-reactors

🔑 Keywords

- small modular reactors

- SMR investment trends

- advanced nuclear energy

- SMR vs renewables

- clean firm power

- modular nuclear reactors

- TerraPower Natrium

- GE Hitachi BWRX-300

- Rolls-Royce SMR

- SMRs and AI data centers

- SMR market forecast

- low-carbon energy infrastructure

- nuclear energy for hydrogen

- next-gen energy technologies

- Microsoft Oklo nuclear deal

- energy transition investment

- decentralized nuclear power

- SMR deployment timeline

- net-zero energy strategy

- energy for hyperscale compute

⚠️ Investment Disclaimer

The information presented in this portfolio allocation is for informational and educational purposes only and does not constitute financial, investment, or legal advice. It is not intended as a recommendation to buy, sell, or hold any securities or investment products. The allocation model reflects general market trends and publicly available research at the time of writing, and may not be suitable for all investors. Please consult with a licensed financial advisor or professional before making any investment decisions.