Robot Economies Are Here: The Surprising Impact of Smart Automation on Labor and GDP

The age of robot economies has arrived. What was once the realm of science fiction—factories run by machines, self-driving trucks, algorithmic managers—is now actively reshaping how labor, productivity, and economic value are defined. Across industries, smart automation is replacing repetitive human tasks, augmenting decision-making, and driving GDP growth in ways that challenge traditional economic models.

From Amazon’s robot-staffed fulfillment centers to autonomous tractors plowing fields in the Midwest, the shift isn’t theoretical—it’s operational. As robotics and AI converge, we are entering an era where capital, not labor, drives growth, and where machines are no longer just tools—they’re economic actors.

But with these gains come trade-offs: job polarization, inequality, and policy lag. This blog explores how robot economies are restructuring labor markets, altering GDP dynamics, and forcing a global rethink on how to sustain prosperity when intelligent systems do most of the work.

The Automation Surge: How Smart Machines Are Transforming Every Sector

The spread of smart automation is no longer confined to factory floors. It’s now transforming virtually every sector of the global economy—replacing repetitive human tasks, boosting productivity, and enabling operations that were previously unimaginable or cost-prohibitive.

In manufacturing, robotic arms and AI-driven quality control systems are enabling 24/7 production with minimal human oversight. Companies like Foxconn and Tesla use intelligent robots to speed up assembly, reduce error rates, and scale output on demand. In logistics, Amazon alone operates over 750,000 robots in its warehouses to optimize picking, sorting, and inventory management—reducing delivery times and labor costs.

In agriculture, autonomous tractors, drones, and robotic harvesters are addressing labor shortages while increasing precision in planting and spraying. Retail and hospitality are also adapting: cashierless stores, robot waiters, and automated kiosks are becoming mainstream in Asia, North America, and parts of Europe.

Even healthcare and construction—traditionally human-intensive sectors—are seeing an influx of automation. Surgical robotics, AI triage systems, and exoskeleton-assisted labor represent a paradigm shift from manual to hybrid labor models.

What ties these sectors together is not just automation, but smart automation: systems that learn, adapt, and operate in complex environments with minimal supervision. This is the true foundation of the robot economy—intelligent systems executing work faster, safer, and at a scale beyond human capability.

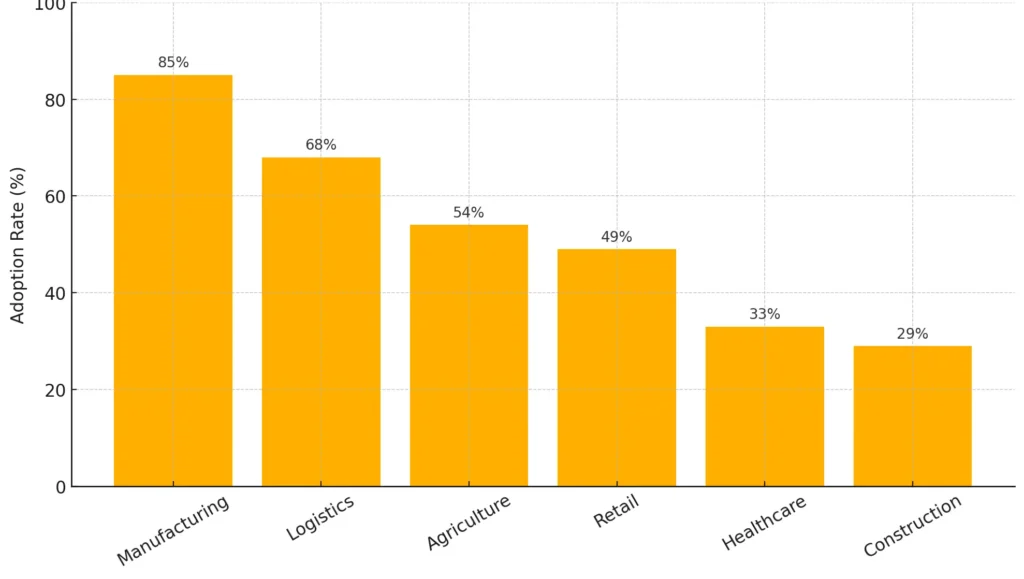

📊 The chart below illustrates the current adoption rate of automation across major industries, highlighting where the robot economy is gaining the strongest traction.

Labor Disrupted: What Jobs Are Disappearing—and Which Ones Are Being Born

Automation isn’t just changing how work is done—it’s reshaping who does the work. In robot economies, labor markets are being restructured in real time. As machines become faster, more precise, and increasingly intelligent, they are overtaking tasks traditionally performed by humans—especially in mid-skill, rule-based roles.

Jobs disappearing include:

- Assembly line operators replaced by robotic arms

- Warehouse pickers displaced by autonomous mobile robots (AMRs)

- Cashiers and clerks replaced by automated kiosks and checkout-free stores

- Truck and delivery drivers, as driverless fleets expand

Meanwhile, entirely new jobs are being born:

- AI model trainers and prompt engineers

- Robot fleet technicians and maintenance experts

- Algorithm auditors and AI ethicists

- Human-machine collaboration designers (e.g., cobot integration specialists)

This shift is creating a barbell-shaped labor market—high demand at the top (AI engineers, data scientists) and bottom (low-wage, non-automatable service roles), while the middle collapses. The result? Wage polarization and a growing divide between those who work with machines and those who are replaced by them.

Reskilling is crucial, but often lags behind the speed of displacement. In robot economies, survival is less about doing repetitive work and more about learning how to design, manage, or coexist with automation.

The New Economics of Automation: How Robot Economies Reshape GDP

In robot economies, the engine of economic growth is no longer human labor alone—it’s smart machines. The traditional link between employment and output is weakening, as automation allows companies to generate more value with fewer people. This shift is not just technological—it’s structural, and it’s reshaping how GDP is formed, measured, and interpreted.

At the heart of this transformation is the capital-labor inversion. In many industries, the share of GDP generated by labor is shrinking, while the contribution from capital—robotic systems, AI software, and digital infrastructure—is growing. Robots don’t draw salaries, don’t sleep, and don’t strike. As a result, businesses are leaning harder into automation to drive output and profit margins.

For example, highly automated sectors like semiconductor manufacturing and e-commerce logistics are seeing soaring productivity rates, even as workforce sizes plateau or decline. In these robot economies, GDP may continue to rise, but traditional metrics like “GDP per worker” are becoming misleading. The output is increasingly produced by machine labor, not human hands.

To stay relevant, some economists are now exploring alternative measures—like GDP per machine-hour, hybrid productivity indices, or even “AI-adjusted growth”—that better reflect the new dynamics of smart automation-driven value creation.

Global Frontlines: Who’s Leading the Smart Automation Race?

Robot economies are not unfolding evenly—they’re accelerating in some countries while lagging in others, based on national policy, industrial priorities, and cultural readiness. A few standout nations are shaping the global trajectory of smart automation.

🇯🇵 Japan leads in social robotics and industrial precision. Facing a rapidly aging population and labor shortages, it has pioneered the use of humanoid robots in elder care and advanced robotics in electronics and auto manufacturing.

🇰🇷 South Korea boasts the highest robot density in the world—over 1,000 robots per 10,000 manufacturing workers. The government-backed K-Humanoid Alliance aims to commercialize general-purpose humanoid robots by 2028.

🇺🇸 The United States relies on private-sector dynamism. Companies like Amazon, Tesla, Boston Dynamics, and NVIDIA drive innovation in warehouse automation, autonomous vehicles, and AI-powered robotics—though regulatory frameworks lag.

🇪🇺 The European Union is taking a human-centric, ethics-first approach. The EU AI Act regulates high-risk automation while funding collaborative robotics and worker retraining through Horizon Europe.

🇨🇳 China has taken a state-led approach. Backed by its “Made in China 2025” initiative and the New Generation AI Development Plan, it has become the world’s largest buyer and deployer of industrial robots. Its focus: scale, speed, and vertical integration—from factories to delivery drones.

Each country’s path reflects a unique response to robot economies—balancing innovation, labor displacement, and national competitiveness.

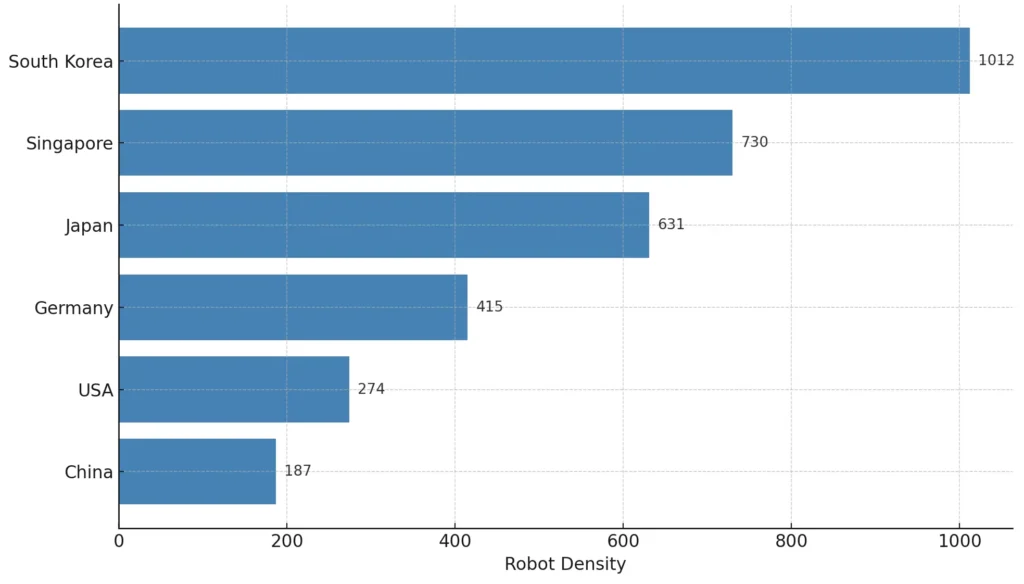

📊 The bar chart below highlights the global leaders in robot economies by robot density, measured as the number of robots per 10,000 manufacturing workers. It underscores the intensity of automation adoption in key nations shaping the future of work.

Winners, Losers, and the Widening Inequality Gap in Robot Economies

As robot economies accelerate, they are creating new divides—between those who benefit from automation and those who are displaced or excluded. The gains are real, but so are the asymmetries.

On the winning side are:

- Tech-savvy professionals who build, operate, or integrate robotics and AI

- Capital owners and firms that scale output through automation

- Cities and regions with strong infrastructure, innovation ecosystems, and reskilling programs

On the losing side are:

- Mid-skill workers displaced by automation in logistics, manufacturing, and retail

- Small businesses unable to afford automation investments

- Rural and aging regions that lack digital infrastructure or training pipelines

The result is a deepening polarization in wages, opportunity, and regional prosperity. Automation drives profits, but without redistributive policies or inclusive strategies, those profits tend to concentrate in a few hands.

This isn’t just about income—it’s about economic mobility. In robot economies, inequality is shaped not only by education or geography, but by access to technology and adaptation speed. The risk is not mass unemployment—but a new underclass excluded from the productivity gains of automation.

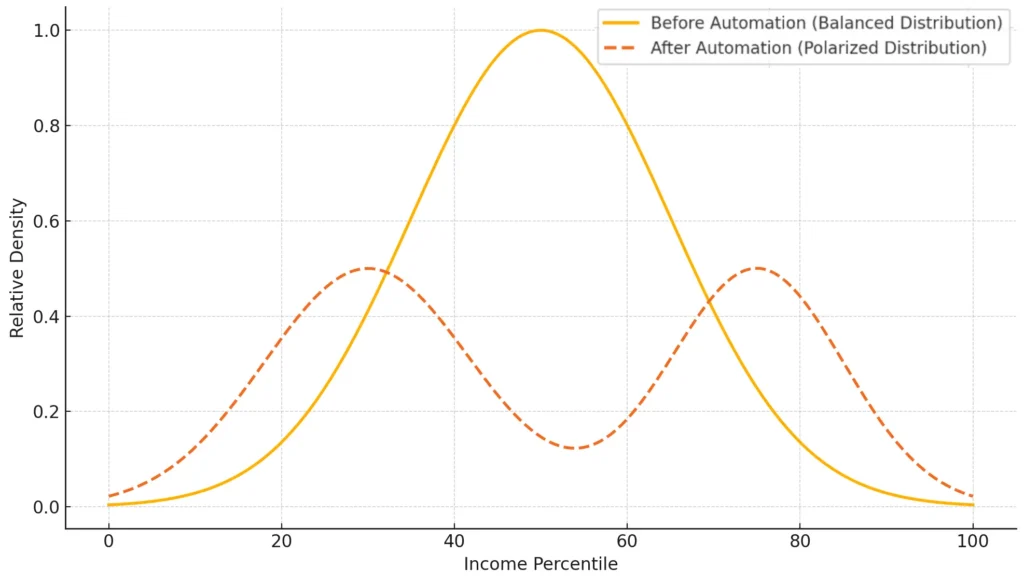

📊 The chart below compares income distribution before and after widespread automation, illustrating how the middle class shrinks while wealth accumulates at the top and lower-wage service work expands at the bottom—a signature pattern in emerging robot economies.

Policy Responses: Can We Make Smart Automation Work for Everyone?

The rise of robot economies presents a pivotal policy challenge: how to harness the gains of automation while minimizing its social fallout. Governments, institutions, and corporations face mounting pressure to redesign labor, education, and tax systems for an era where machines do much of the work.

One response is reskilling at scale. Countries like Singapore and Germany are investing in lifelong learning programs and vocational tech education to help workers transition into AI, robotics, and advanced manufacturing roles. Public-private initiatives are emerging to fund upskilling pipelines tied to local labor market needs.

Another approach is redistribution. Proposals range from automation taxes (taxing companies that replace human workers with machines) to Universal Basic Income (UBI) trials that decouple livelihood from employment. While controversial, these models acknowledge that productivity may no longer require full employment.

In parallel, corporate responsibility is growing. Forward-looking companies are building in-house retraining programs and human-robot collaboration strategies instead of mass layoffs.

Ultimately, policy must evolve from reactive to proactive. In robot economies, the question isn’t just how to protect jobs—but how to equip citizens to thrive in a world where machines are co-workers, not replacements.

Growth Without Jobs? Rethinking Productivity and Prosperity

In robot economies, a paradox is emerging: economic growth without parallel job growth. Thanks to automation, companies can scale output, boost efficiency, and grow profits—without hiring more workers. In fact, many are growing faster by reducing headcount and investing in intelligent machines.

This phenomenon, often referred to as decoupling, marks a historic break from the labor-output relationship that defined industrial economies. Traditionally, GDP expansion meant more jobs. Now, productivity is increasingly powered by machines, not manpower.

The implications are profound. Can an economy remain consumption-driven if a large share of its population isn’t earning wages? Can governments sustain social services when fewer people contribute income taxes? If machines create the value, who owns it—and who benefits?

Robot economies may force us to rethink core assumptions: that work equals worth, that jobs equal income, and that growth benefits all. Without policy and ownership reform, we risk building systems where productivity soars—while prosperity narrows.

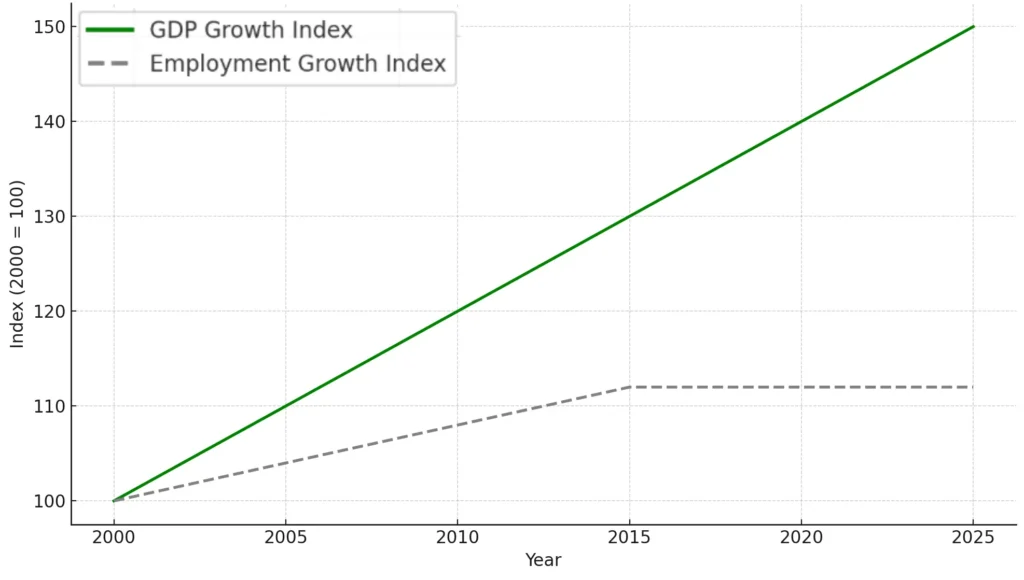

📊 The chart below illustrates the decoupling of GDP and employment, revealing how output continues to rise even as job growth flattens—a central paradox of the smart automation age.

Future Scenarios: What Happens When Machines Handle Most of the Work?

As robot economies mature, we face a defining question: What kind of society do we build when machines do most of the work? The answer depends less on the technology—and more on the choices we make.

🟥 Scenario 1: Collapse

In this trajectory, automation deepens inequality, erodes job markets, and outpaces public policy. Social unrest grows as wealth concentrates in tech-owning elites and millions are left behind. Trust in institutions declines.

🟨 Scenario 2: Control

Governments step in to tightly regulate automation, enforce job guarantees, or restrict tech deployment. Growth slows but stability is maintained. Innovation is bounded by social safeguards—possibly at the cost of competitiveness.

🟩 Scenario 3: Collaboration

The most optimistic future: humans and machines work together in a hybrid economy. New jobs emerge in creativity, caregiving, governance, and AI oversight. Wealth generated by automation is shared through public investment, stakeholder capitalism, or digital dividends.

These paths aren’t mutually exclusive—but the balance we strike between efficiency, equity, and purpose will determine whether robot economies elevate or divide us.

Conclusion: Preparing for a World Where Robot Economies Are the Norm

Robot economies aren’t coming—they’re here. From smart factories and autonomous fleets to AI-managed workflows, automation is already reshaping how we produce, earn, and grow. The question is no longer if automation will change the economy—it’s who will shape what comes next.

Investors, policymakers, business leaders, and workers each have a role in navigating this transition. The challenge is not to stop automation, but to steer it—toward outcomes that enhance productivity and equity.

If we get it right, robot economies won’t just reduce costs—they’ll free up human potential. But if left unchecked, they could widen divides we’re already struggling to close.

The time to act is now.

📚 References

- World Economic Forum. (2023). Future of Jobs Report 2023.

https://www.weforum.org/reports/future-of-jobs-report-2023 - McKinsey Global Institute. (2023). The economic potential of generative AI: The next productivity frontier.

https://www.mckinsey.com/mgi/overview/2023-economic-potential-of-generative-ai - International Federation of Robotics. (2024). World Robotics Report: Global Robot Installations Reach All-Time High.

https://ifr.org/ifr-press-releases - OECD. (2022). Automation, digitalisation and platforms: Implications for work and employment.

https://www.oecd.org/employment/automation-and-employment.htm - IMF. (2023). The Rise of Artificial Intelligence: Implications for Labor and Inequality.

https://www.imf.org/en/Publications/WP/Issues/2023/08/01/Rise-of-AI-and-Labor-Inequality - Statista. (2024). Robot Density in Manufacturing Industries by Country.

https://www.statista.com/statistics/1177085/global-robot-density-by-country/ - European Commission. (2024). EU AI Act: A Human-Centric Approach to Artificial Intelligence.

https://digital-strategy.ec.europa.eu/en/policies/european-approach-artificial-intelligence - MIT Technology Review. (2023). The Productivity Trap: Why Robots Aren’t Creating Enough Jobs Yet.

https://www.technologyreview.com/2023/11/15/productivity-trap-robots-labor-jobs/

🔑 Recommended Meta Keywords

- robot economies

- automation and labor markets

- impact of robots on GDP

- automation and economic growth

- future of work

- AI and job displacement

- smart automation

- capital vs labor shift

- GDP automation trends

- robot density by country

- economic impact of automation

- productivity and automation

- automation inequality

- reskilling for robot economies

- future of jobs in AI era

⚠️ Investment Disclaimer

The information presented in this portfolio allocation is for informational and educational purposes only and does not constitute financial, investment, or legal advice. It is not intended as a recommendation to buy, sell, or hold any securities or investment products. The allocation model reflects general market trends and publicly available research at the time of writing, and may not be suitable for all investors. Please consult with a licensed financial advisor or professional before making any investment decisions.