10 Emerging Technologies Every Investor Should Watch Before 2026

Why 2026 Matters for Tech Investors

The next wave of wealth creation won’t come from traditional industries—it will emerge from breakthrough technologies that redefine how economies function. As we approach 2026, innovation is no longer linear. AI models are writing code, robots are replacing warehouse workers, and biotech firms are engineering living systems like software. Investors who grasp these tectonic shifts early stand to benefit from exponential growth—not just marginal returns.

The investment world is paying attention. Sequoia Capital recently stated, “We believe the next 10,000 unicorns won’t be apps—they’ll be AI agents, climate solutions, and biology-based platforms.” Meanwhile, BlackRock’s 2024 outlook identifies emerging tech sectors like clean energy, healthcare AI, and custom semiconductors as “critical to both economic resilience and alpha generation.” Capital is flowing not just into moonshots, but into scalable, real-world applications with visible ROI pathways.

This blog highlights 10 emerging technologies every investor should watch before 2026—not hype trends, but strategic domains backed by institutional momentum, commercial readiness, and policy tailwinds. For each technology, we’ll break down what it is, why it matters, where capital is flowing, and how you can position yourself now—before the rest of the market catches on.

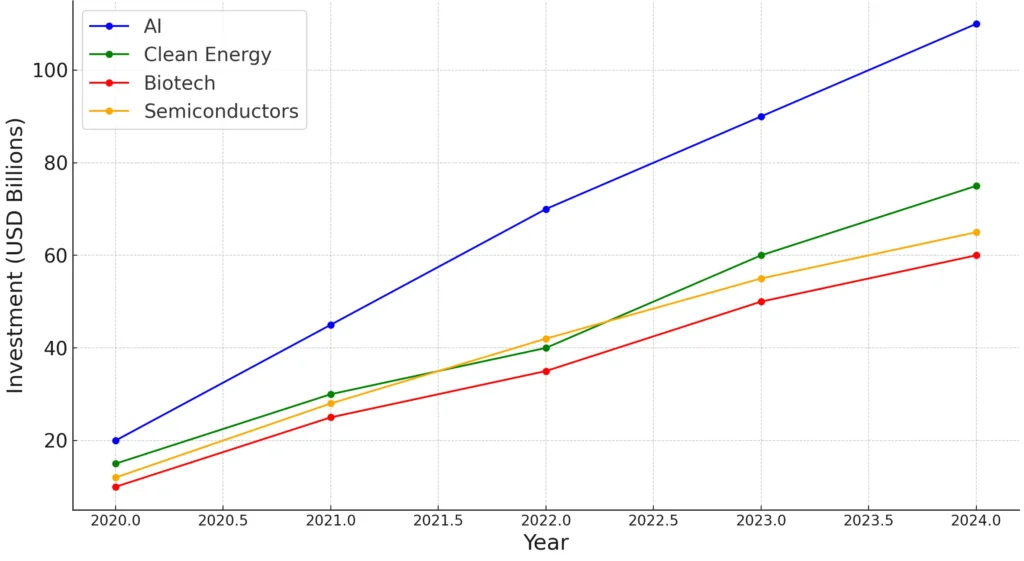

Here is the line chart showing the growth of global VC and institutional investments from 2020 to 2024, broken down into four key emerging technology sectors: AI, clean energy, biotech, and semiconductors. AI leads the surge, but all sectors show strong upward momentum—ideal for highlighting institutional confidence in your blog.

How to Identify ‘Investor-Ready’ Technologies

Not all emerging technologies are investable. Some are still confined to research labs, others are caught in regulatory limbo, and many are riding hype cycles without a clear path to revenue. So how can investors distinguish between bold ideas and bankable innovation?

The key is to focus on “investor readiness”—a set of signals that indicate whether a technology is moving beyond prototypes and gaining real-world traction. These signals include:

- Scalability: Is the tech built for mass adoption or still stuck in niche use cases?

- Commercial Deployment: Are enterprise customers, governments, or consumers actually using it?

- Capital Inflows: Is the technology attracting funding from top VCs, institutional investors, or strategic corporates?

- Regulatory Momentum: Is the policy landscape becoming more supportive (e.g., energy credits, FDA fast-tracking, AI frameworks)?

- Ecosystem Maturity: Are suppliers, tools, talent, and complementary infrastructure in place?

Take the example of solid-state batteries. Just a few years ago, they were a speculative bet. Today, Toyota and QuantumScape are running pilot lines, and government subsidies are flowing into next-gen energy storage. That’s investor-ready.

By applying this lens, investors can filter out the noise and double down on technologies that not only promise disruption—but also deliver returns within realistic timeframes.

Let’s break down the 10 emerging technologies every investor should be watching now.

1. AI Agents & Foundation Models

Artificial intelligence has shifted from assistance to autonomy. The era of AI agents—autonomous software systems capable of reasoning, decision-making, and taking action—is no longer speculative. These agents go beyond static chatbots. They can schedule meetings, analyze financial statements, conduct research, write code, and even coordinate with other agents in complex workflows.

This leap is powered by foundation models—massive AI models like OpenAI’s GPT-4, Google Gemini, Meta LLaMA, and Mistral. What’s different now is the rise of agent frameworks like Auto-GPT, Devin, and OpenAI’s Assistants API, which turn these models into task-completing digital workers. They are being embedded into enterprise systems, operating as virtual employees across sales, HR, coding, customer support, and data analysis.

From an investor perspective, the implications are huge. McKinsey estimates that AI agents could automate work equivalent to up to 30% of all hours across the U.S. economy by 2030. Sequoia, Andreessen Horowitz, and Tiger Global are pouring capital into agent-based startups. Microsoft and Amazon are integrating agents into their cloud ecosystems. For public market exposure, companies like Palantir, ServiceNow, Salesforce, and Nvidia offer indirect plays through enterprise adoption and infrastructure provisioning.

The agent economy isn’t a fringe trend—it’s becoming a core layer of the global workforce. Investors should closely track how fast these systems are moving from experimental to indispensable.

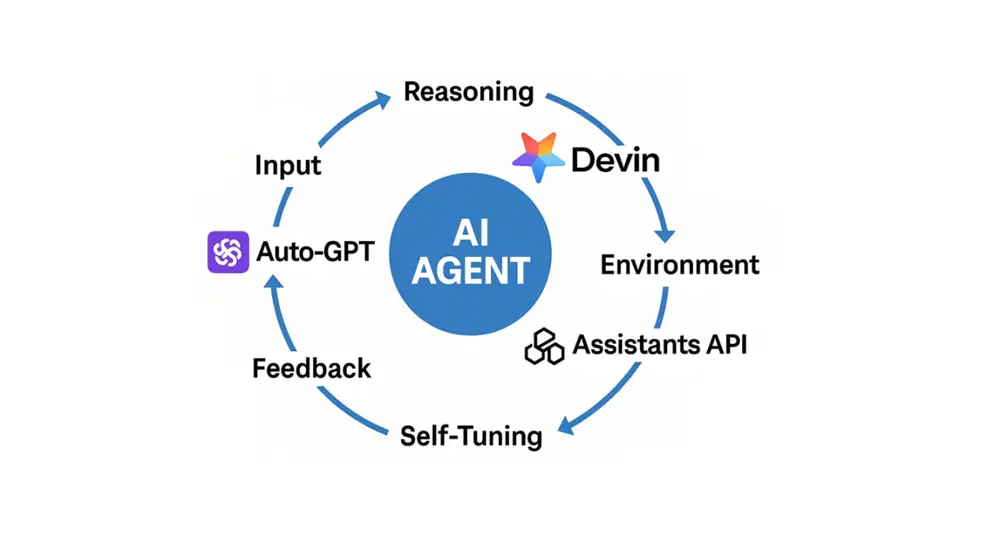

Below is the AI Agent Feedback Loop, the foundational mechanism that enables autonomous AI to learn, adapt, and act in real-world contexts.

2. AI Chips & Edge Computing Architectures

The AI revolution is running into a silicon bottleneck. Large models like GPT-4 and Gemini require immense computational power—driving explosive demand for high-performance chips. While Nvidia has dominated the AI chip market with its H100 and upcoming Blackwell GPUs, a deeper shift is underway: the rise of custom silicon and edge AI architectures.

Tech giants like Google (TPU), Amazon (Inferentia), Apple (Neural Engine), and Meta (MTIA) are now designing purpose-built AI chips optimized for inference, power efficiency, and proprietary workloads. These chips reduce costs, improve latency, and ensure control over the AI stack. At the same time, edge AI chips—from players like Qualcomm, Tenstorrent, and AMD—are enabling real-time decision-making in cars, devices, cameras, and factories without relying on cloud data centers.

This isn’t just about performance—it’s about strategic independence and vertical integration. Companies are moving from general-purpose GPUs to domain-specific accelerators that unlock new applications, especially in robotics, autonomous vehicles, and IoT.

From an investor’s perspective, this sector is a goldmine. While Nvidia remains the flagship play, rising contenders like TSMC, Broadcom, ARM, and Marvell are gaining traction. For diversified exposure, ETFs such as the VanEck Semiconductor ETF (SMH) and iShares Semiconductor ETF (SOXX) are solid entry points.

For early-stage opportunities, keep an eye on startups like Groq and Cerebras, which are developing purpose-built architectures optimized for large-scale AI inference.

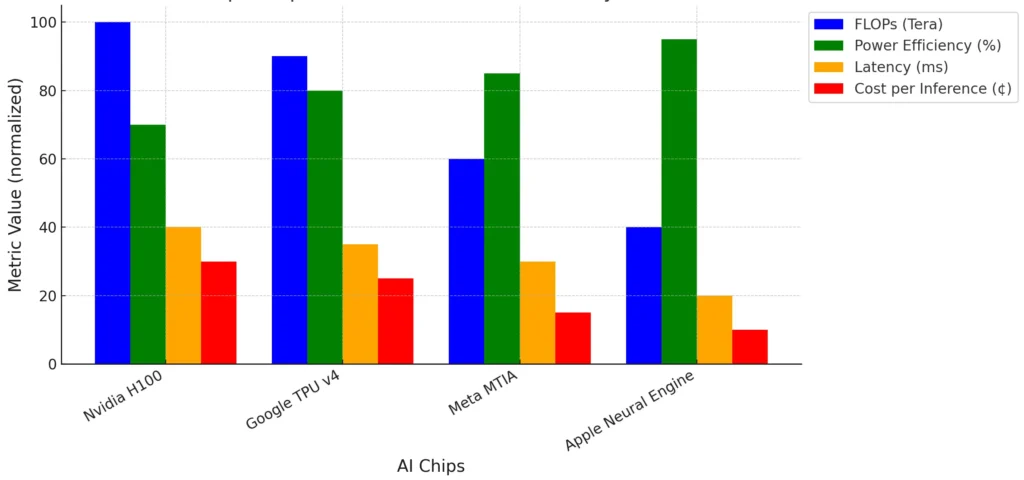

The bar chart below compares key performance and efficiency metrics across today’s leading AI chips.

3. Robotics & Autonomous Systems

Robotics has officially moved beyond the lab—and into the factory, the warehouse, the hospital, and even the battlefield. As labor shortages, logistics disruptions, and manufacturing inefficiencies become more acute, autonomous systems are stepping in to fill the gap. From robotic arms in fulfillment centers to surgical robots and autonomous delivery vehicles, the robotics industry is quietly becoming one of the fastest-growing AI-powered sectors.

The key shift is the fusion of AI with robotics. No longer rigid machines executing pre-programmed tasks, today’s robots use computer vision, machine learning, and sensor fusion to make real-time decisions in unstructured environments. Boston Dynamics’ Atlas can now navigate construction sites, Amazon deploys fleets of mobile robots in its warehouses, and Hyundai is building next-gen factories powered by humanoid machines.

Strategically, the most attractive plays are not just the robots themselves, but the infrastructure surrounding them—from chipsets and servos to software platforms and SLAM algorithms. Companies like ABB, Rockwell Automation, Zebra Technologies, and Nvidia (through its Isaac platform) are building scalable, modular systems that can be deployed across sectors.

Investors should also watch robotics-focused ETFs such as the Global X Robotics & AI ETF (BOTZ) and the ROBO Global Robotics & Automation Index ETF (ROBO), which provide diversified exposure to this rapidly growing market.

At the same time, venture capital is pouring into vertical robotics startups—from Locus in logistics to Naio in agriculture and Simbe in retail automation.

The photo below captures a delivery robot in action, showcasing how robotics is already reshaping last-mile operations on urban streets.

4. Battery Tech & Energy Storage Innovation

The transition to electric vehicles, renewable grids, and energy-resilient infrastructure hinges on one linchpin: better batteries. The global demand for efficient, safe, and scalable energy storage is driving an innovation surge—from lithium-iron-phosphate (LFP) and sodium-ion to the holy grail: solid-state batteries.

Traditional lithium-ion batteries are reaching their limits in energy density and fire risk. In contrast, solid-state batteries use solid electrolytes, enabling faster charging, higher capacity, and improved safety. Toyota, QuantumScape, and CATL are racing to bring solid-state technology to mass production, while government subsidies in the U.S., EU, and Asia are accelerating pilot deployments.

Meanwhile, sodium-ion batteries are gaining attention for grid-scale storage due to their low cost and raw material abundance. Companies like BYD and Faradion are advancing commercial viability, especially in stationary applications where energy density is less critical than price and stability.

For investors, battery innovation is not just a materials play—it’s a platform shift driving the future of mobility, energy, and infrastructure.

Exposure opportunities include public equities like Albemarle (a leading lithium supplier), Panasonic, and QuantumScape, as well as thematic ETFs such as LIT (Global X Lithium & Battery Tech) and BATT (Amplify Advanced Battery Metals & Materials).

To build a comprehensive position, investors should monitor both upstream activities—such as mining and refining—and downstream deployment in sectors like electric vehicles and grid-scale storage.

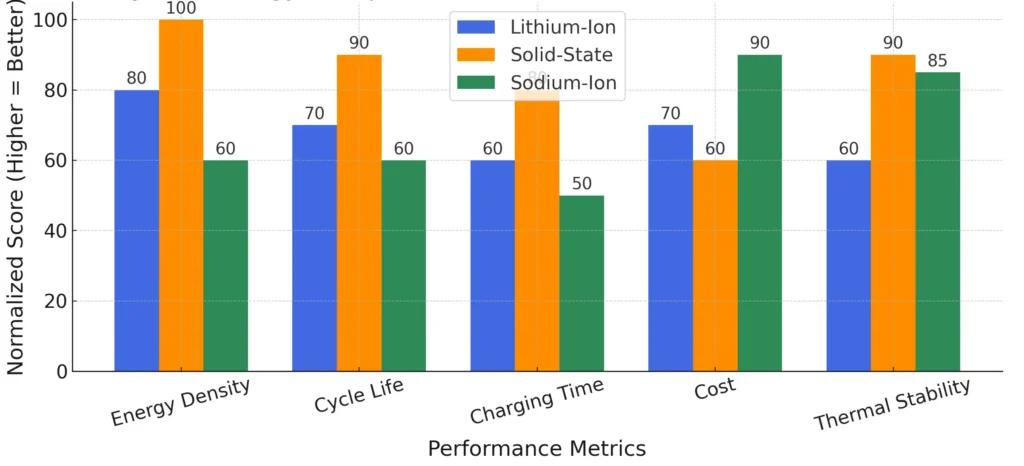

The bar chart below compares the core performance metrics of Lithium-Ion, Solid-State, and Sodium-Ion batteries, highlighting their relative strengths in energy density, cost, cycle life, and safety.

5. Small Modular Reactors (SMRs) & Nuclear Tech Reinvented

Nuclear energy is making a comeback—but not in the form most people expect. Rather than massive, slow-to-build power plants, the future belongs to Small Modular Reactors (SMRs)—compact, factory-built nuclear systems designed to be safer, faster to deploy, and more cost-effective.

SMRs are reshaping the nuclear narrative. Companies like TerraPower (backed by Bill Gates), NuScale Power, GE Hitachi, and X-energy are leading efforts to deploy reactors that can be assembled off-site and shipped like industrial equipment. These reactors promise consistent baseload power, smaller environmental footprints, and passive safety features—solving many of the public perception and regulatory hurdles that have plagued traditional nuclear.

Governments are backing this shift. The U.S. Department of Energy has allocated billions to SMR pilot projects. The UK, Canada, and South Korea have also prioritized SMRs in their national energy strategies. As the world transitions from fossil fuels, SMRs could fill the reliability gap that solar, wind, and batteries alone can’t cover.

For investors, this sector offers both direct and indirect plays. NuScale (SMR) is already publicly listed. Others like BWX Technologies (BWXT), Fluor Corp (FLR), and Cameco (CCJ) offer exposure to the broader nuclear supply chain. ETFs like URA (Global X Uranium ETF) and NLR (VanEck Uranium+Nuclear Energy ETF) track companies positioned to benefit from next-gen nuclear deployment.

6. AI in Healthcare & Biopharma

No industry is being transformed by AI more urgently—or more significantly—than healthcare. With aging populations, clinician shortages, and rising R&D costs, the sector is ripe for disruption. AI is stepping in to streamline diagnosis, accelerate drug discovery, personalize treatment, and automate clinical workflows.

AI-powered tools are already outperforming radiologists in detecting tumors, predicting patient deterioration, and modeling disease progression. Companies like Tempus AI, Butterfly Network, and PathAI are leading in diagnostics, while firms like Insilico Medicine and Recursion Pharmaceuticals use generative AI to model proteins and discover new compounds—slashing drug development timelines and costs.

From an investment perspective, the field spans both biotech and software infrastructure. Tech giants like Google Health and Amazon Web Services for Health are building platforms to host and process sensitive medical data, while health-focused AI startups are securing massive rounds from strategic investors. The FDA has already approved dozens of AI-assisted medical devices, signaling growing regulatory acceptance.

Public investors can gain exposure to this accelerating trend through companies like Teladoc, IQVIA, and Moderna, which actively integrates AI in its mRNA development pipeline. Broader access is also available through thematic ETFs such as IBB (iShares Nasdaq Biotechnology ETF) and HTEC (Robo Global Healthcare Tech & Innovation ETF).

However, some of the most promising opportunities lie at the intersection of AI infrastructure, pharmaceutical R&D, and cloud-based healthcare platforms—where innovation is rapidly compressing discovery timelines and unlocking new therapeutic models.

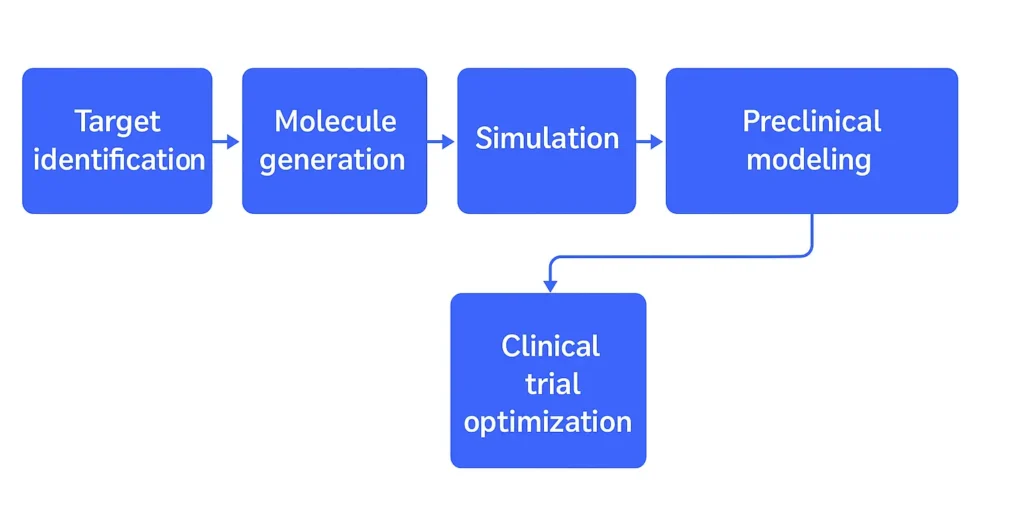

The flowchart below visualizes how AI enhances each stage of the drug development pipeline—from target identification and molecule generation to simulation, preclinical modeling, and clinical trial optimization. By streamlining these historically time-intensive processes, AI can significantly reduce R&D costs, accelerate time to market, and raise the probability of clinical success.

7. Synthetic Biology & Biofabrication

Synthetic biology is no longer science fiction—it’s a new industrial platform. By treating DNA like software, scientists can now program cells to manufacture fuels, materials, food, and medicine with remarkable precision and sustainability. Think of it as biotechnology 2.0—where microbes are engineered to operate like microscopic factories.

The field is advancing rapidly across multiple industries:

- In biomanufacturing, companies like Ginkgo Bioworks and Zymergen engineer microbes to produce fragrances, chemicals, and enzymes.

- In food tech, firms such as Upside Foods and Perfect Day grow meat and dairy from cells without animals.

- In sustainable materials, startups are producing spider silk, leather, and biodegradable plastics in lab-controlled environments.

What makes this especially investable now is the platform shift toward modular, programmable, and scalable biofactories. AI and robotic automation are accelerating design-build-test cycles, slashing the time it takes to optimize organisms for industrial output. Governments and corporates are heavily backing biofoundries to localize supply chains and reduce fossil-fuel dependency.

For investors, public exposure remains limited but growing. Ginkgo Bioworks (DNA) is a bellwether, while Amyris, Codexis, and Danaher offer indirect plays. The ARK Genomic Revolution ETF (ARKG) includes several synthetic bio leaders. Private VC investment remains strong in food-tech and industrial bio, with exits through SPACs and M&A gaining momentum.

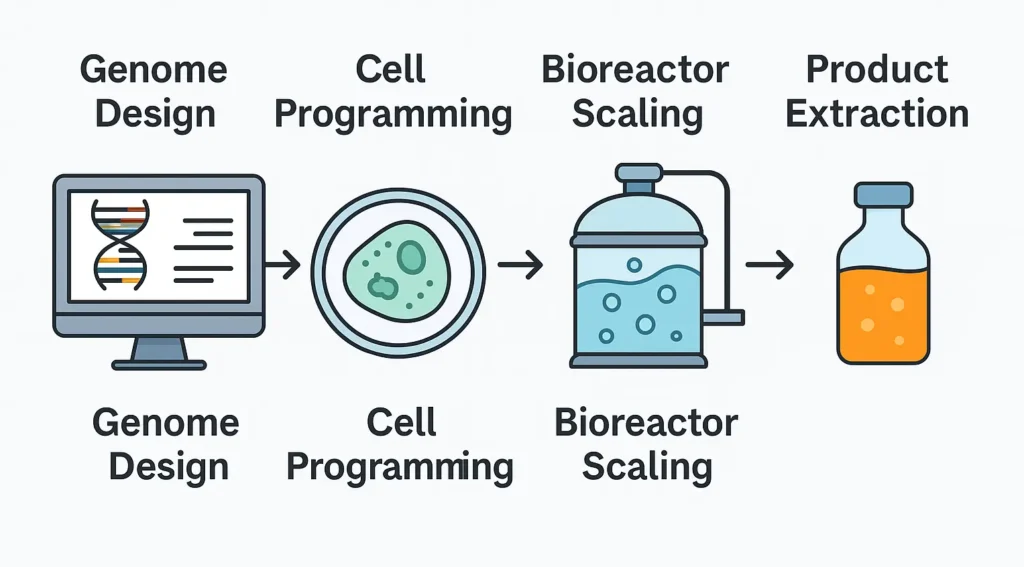

The mockup below illustrates the biofactory pipeline—a streamlined path from lab bench to industrial output. It begins with genome design, where biological blueprints are created digitally. These are then used in cell programming, where microbes are engineered to perform specific functions, such as producing enzymes or fuels.

In the next phase, bioreactor scaling, these modified cells are multiplied under controlled conditions to achieve industrial-scale yields. Finally, the desired compounds are recovered through product extraction.

This end-to-end pipeline is central to the promise of synthetic biology: transforming biology into a programmable, scalable platform for sustainable manufacturing.

8. Spatial Computing & the Industrial Metaverse

Spatial computing—the fusion of digital and physical environments—is rapidly evolving from a buzzword into a practical toolset powering everything from immersive training to factory optimization. It includes technologies like augmented reality (AR), digital twins, 3D simulation, and context-aware AI—all working together to turn the physical world into programmable infrastructure.

This isn’t just about VR headsets or gaming. Companies are using digital twins to model entire manufacturing facilities, detect bottlenecks in real time, and simulate failure scenarios before they happen. In logistics, AR headsets overlay instructions and alerts directly onto workers’ fields of view, increasing speed and safety. In healthcare, spatial interfaces help surgeons visualize anatomy before making an incision.

The big push is coming from enterprise players:

- Apple Vision Pro is positioning spatial computing as the next productivity platform.

- Siemens, PTC, and NVIDIA Omniverse are leading in industrial and engineering applications.

- Unity and Matterport are building the spatial layer for retail, real estate, and digital walkthroughs.

For investors, spatial computing spans a diverse set of sectors—from hardware makers like Apple and Qualcomm, to software platforms such as Unity and Autodesk, and enterprise-focused B2B SaaS providers like PTC and Bentley Systems.

ETFs including XR (SPDR S&P Kensho Future Security ETF) and ROBO offer diversified exposure to companies operating at the crossroads of automation, 3D simulation, and spatial intelligence.

Although still in the early stages of adoption, its enterprise-first momentum—especially in manufacturing, engineering, and logistics—makes spatial computing a trend with immediate investability.

The image below shows a factory worker using an AR headset to inspect a machine, with real-time performance data displayed in a digital overlay—demonstrating how spatial tech enhances on-site productivity and decision-making.

9. Quantum Computing: Where Are We Now?

Quantum computing is one of the most hyped—and misunderstood—emerging technologies. While headlines promise that quantum will “break encryption” and “revolutionize science,” the current reality is more measured. Still, major breakthroughs are happening in hardware stability, error correction, and cloud accessibility, bringing us closer to practical applications.

Companies like IBM, Google, and Rigetti are racing to scale up qubit counts while reducing noise. Meanwhile, D-Wave is already commercializing quantum annealing for optimization problems. Amazon and Microsoft are offering quantum-as-a-service platforms through their cloud ecosystems, allowing developers and researchers to test algorithms without building hardware.

What makes quantum computing exciting is its unique ability to solve problems that classical computers struggle with—like molecular simulation, supply chain optimization, and cryptography. For now, most use cases are in research and proof-of-concept pilots, but industries like pharmaceuticals, logistics, and finance are investing heavily in preparation for real-world deployment.

From an investor standpoint, this is a long-horizon bet. Public exposure includes IonQ (IONQ), Rigetti (RGTI), and legacy players like IBM and Honeywell (via Quantinuum). ETFs such as QTUM (Defiance Quantum ETF) or ARKQ offer broader exposure. While mass adoption may be years away, early positioning in quantum infrastructure and software could pay off big in the next computing cycle.

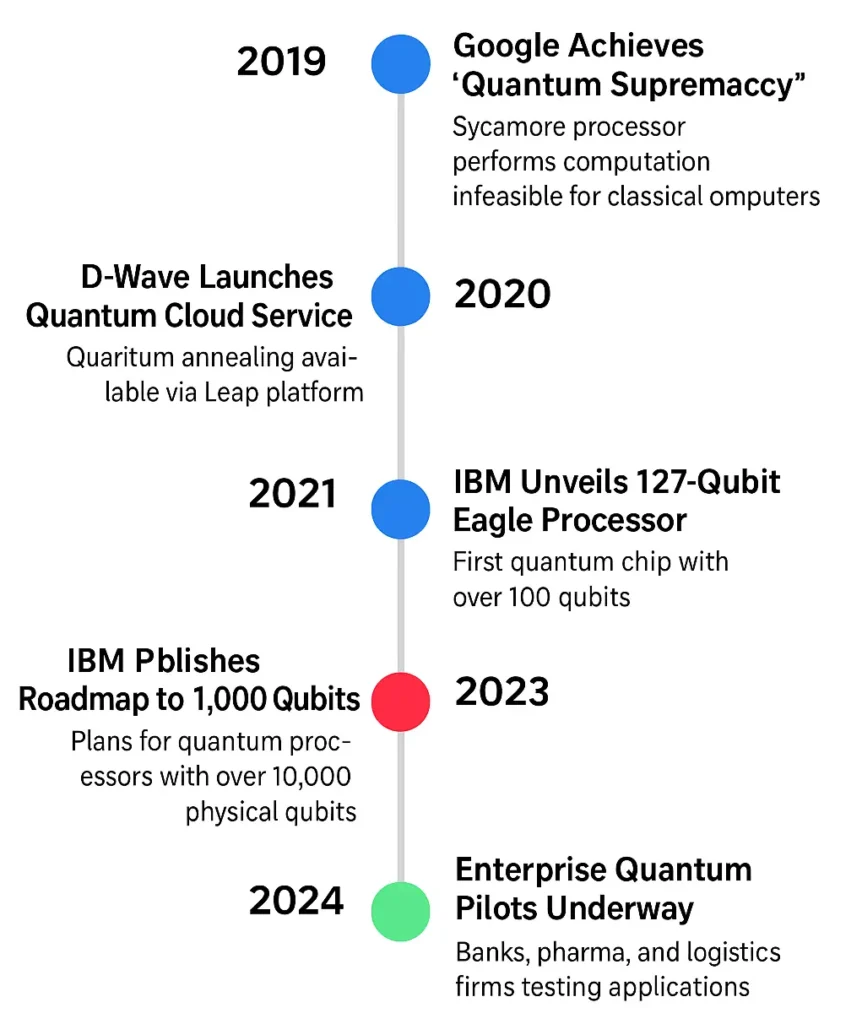

Here is the visual timeline of major quantum computing breakthroughs from 2019 to 2024, showcasing milestones from Google’s quantum supremacy to IBM’s roadmap toward a 1000+ qubit processor. It provides clear chronological context for investors tracking the field’s progress from theory to commercialization.

10. Satellite Internet & the Space Economy

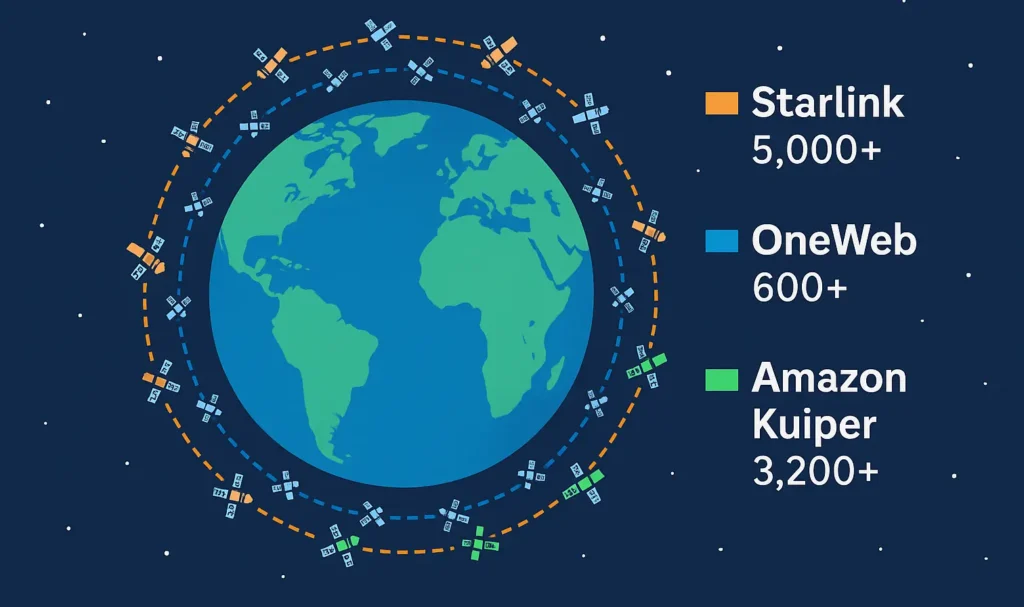

Space is no longer the final frontier—it’s the next economic frontier. The launch of thousands of low-Earth orbit (LEO) satellites by companies like SpaceX, OneWeb, and Amazon Kuiper is building a new layer of internet infrastructure: global, low-latency satellite broadband. This backbone will power remote education, connected vehicles, battlefield communications, and rural commerce.

The most mature application is satellite internet, where SpaceX’s Starlink already operates over 5,000 satellites and serves over 2 million users. But the opportunity extends far beyond connectivity. The broader orbital economy includes space logistics, satellite manufacturing, in-orbit servicing, earth observation, and even early space tourism.

Governments are increasingly involved—not just in regulation, but as customers. The U.S. Department of Defense is integrating LEO broadband into its communications stack. The EU’s IRIS2 satellite network and China’s Guowang constellation reflect growing geopolitical stakes in space infrastructure.

For investors, the space economy blends high-risk frontier tech with high-growth infrastructure opportunities. Direct exposure is available through publicly traded companies such as Iridium (IRDM), Maxar, Rocket Lab (RKLB), and AST SpaceMobile (ASTS). For broader, diversified access, ETFs like ARKX (ARK Space Exploration & Innovation ETF) and UFO (Procure Space ETF) track a wide range of orbital and satellite-focused firms.

Over time, the most valuable players will likely be vertically integrated—combining launch capabilities, satellite deployment, and in-orbit services into a unified stack that supports everything from broadband to Earth observation.

The infographic below compares leading LEO (Low Earth Orbit) satellite constellations by operator—Starlink, OneWeb, and Amazon Kuiper—highlighting satellite count and coverage. These expanding networks are forming the digital backbone of global satellite internet, unlocking connectivity in underserved and remote regions worldwide.

Conclusion

The technologies outlined in this blog—ranging from AI agents and robotics to quantum computing and synthetic biology—aren’t speculative fads. They represent structural transformations that will reshape global industries, markets, and economic power dynamics over the next decade.

What makes this moment different is convergence. AI is not just a standalone trend—it’s a catalyst unlocking advancements in drug discovery, semiconductor design, industrial automation, and even space infrastructure. Meanwhile, advances in energy storage, spatial computing, and biomanufacturing are redefining what’s possible in sectors long thought too slow to disrupt.

For investors, the opportunity lies in strategic positioning. A future-proof portfolio won’t chase hype—it will balance long-horizon innovation bets (quantum, synthetic bio) with near-term platform plays (AI chips, robotics, SMRs). It will combine public equities, thematic ETFs, and ongoing research tracking to anticipate where institutional capital is heading next.

As always, the edge belongs to those who stay ahead of the narrative—and allocate not just capital, but attention, toward the technologies reshaping tomorrow’s economy.

📚 References

- McKinsey & Company. “The Economic Potential of Generative AI: The Next Productivity Frontier.” June 2023.

- Sequoia Capital. “Generative AI Market Map & Investment Outlook.” March 2023.

- Morgan Stanley. “Space: Investing in the Final Frontier.” 2023.

- ARK Invest. “Big Ideas 2024.” January 2024.

- BCG. “How to Win the Quantum Race.” March 2023.

- IBM Quantum Development Roadmap.

- PitchBook. “Emerging Tech Research: Synthetic Biology.” Q2 2023.

- NVIDIA. “Transforming Factories with AI and Robotics.” 2023.

- Statista. “Global Venture Capital Investment in Deep Tech by Sector.” 2024.

- Defiance ETFs. “QTUM – Quantum and Machine Learning ETF.”

🔍 Keywords

emerging technologies 2026, future tech investments, AI investment trends, robotics stocks 2025, quantum computing investment, synthetic biology market, AI chips ETF, spatial computing startups, SMR nuclear energy stocks, biotech AI startups, satellite internet stocks, space economy investing, best tech ETFs 2025, technology portfolio strategy, disruptive tech trends 2025, long-term tech investing, frontier technology 2026, innovation economy analysis, tech investor guide, next big tech sectors

⚠️ Investment Disclaimer

The information presented in this portfolio allocation is for informational and educational purposes only and does not constitute financial, investment, or legal advice. It is not intended as a recommendation to buy, sell, or hold any securities or investment products. The allocation model reflects general market trends and publicly available research at the time of writing, and may not be suitable for all investors. Please consult with a licensed financial advisor or professional before making any investment decisions.