AI Is Replacing Middle Management — Here’s What Investors Should Know

The Silent Revolution in Corporate Leadership

Middle management has long been considered a stable pillar in the corporate hierarchy—essential for coordination, oversight, and execution. But that assumption is being quietly upended. A new class of AI agents is now stepping into roles once dominated by human managers, not only executing repetitive tasks but making real-time decisions, assigning work, evaluating performance, and even delivering feedback. This shift is happening faster than most realize—and it’s already starting to reshape operational structures across industries.

For investors, the implications are profound. The replacement of human managers with autonomous software agents isn’t just about cost-cutting—it signals a structural transformation in how companies create leverage, scale operations, and deliver margin growth. Companies that deploy AI agents can unlock compounding productivity without proportional headcount growth, leading to improved earnings profiles with leaner organizational models. These operational upgrades often go unnoticed in headlines but quietly show up where it matters most: the bottom line.

This blog explores how AI agents are replacing middle management, why this moment matters, and what it means for your holdings. From real-world deployments to financial performance signals, we’ll uncover where this management automation trend is already delivering alpha—and how you can position your portfolio to benefit from this emerging source of digital leverage.

What Are AI Agents—And Why Are They Management-Grade?

More Than Just a Bot

An AI agent is not just a chatbot or task bot—it’s a software system capable of making decisions, taking actions, and managing tasks autonomously. Powered by large language models (LLMs), AI agents can understand natural language, interpret objectives, and coordinate tasks across platforms like Slack, Jira, or Salesforce. Unlike traditional automation, agents handle dynamic, non-linear workflows—exactly the type of work performed by human middle managers.

Why It Matters for Investors

The average middle manager costs between $100,000 to $150,000 annually, while an AI agent—depending on the platform—can operate at $1,000 to $15,000 per year. More importantly, AI agents scale without payroll growth. One agent can oversee multiple workflows simultaneously, with near-zero marginal cost. This means companies can increase operational capacity without adding headcount—creating new forms of software-driven operating leverage.

This has direct implications for SG&A (Selling, General & Administrative) ratios, a key line item for investors. As AI agents replace middle-layer roles, SG&A can shrink even as output grows. Companies integrating agents will likely see early signs of margin improvement long before headlines catch on.

Functional Superiority: Where They Outperform

AI agents excel in areas where precision, consistency, and real-time responsiveness matter. They can:

- Attend virtual meetings and extract action items

- Assign tasks and monitor progress

- Analyze KPIs and trigger alerts

- Escalate risks or delays automatically

Unlike human managers, they don’t suffer from bias, fatigue, or communication delays. They work around the clock and integrate seamlessly into systems—HR platforms, CRMs, ERPs—handling multi-system tasks with full traceability. In effect, they deliver faster decisions with lower friction.

Real Players Embedding Management Agents

This isn’t theoretical. Microsoft’s Copilot assists with email triage, meeting summaries, and task delegation. ServiceNow’s Now Assist automates HR and IT workflows once handled by managers. IBM Watson Orchestrate links agents to core systems for business process execution.

These platforms reduce dependence on human coordination, offering companies greater agility and cost control. For investors, that means watching for companies that are early adopters of agent-enabled infrastructure—they’re likely to benefit from improved margins, faster scaling, and long-term competitive advantage.

Real-World Deployments: AI Agents in Action

Amazon: Automated Warehouse Oversight

Amazon has integrated AI agents deep into its warehouse and logistics systems. These agents handle scheduling, productivity monitoring, shift management, and even performance feedback—functions traditionally overseen by supervisors. This allows Amazon to scale fulfillment operations efficiently without increasing supervisory headcount. The result: faster throughput, tighter operational control, and lower SG&A.

Walmart: Scheduling and Inventory Coordination

Walmart employs AI agents to manage workforce scheduling, resolve staffing conflicts, and optimize inventory coordination in real time. These agents replace functions typically handled by assistant managers or floor supervisors. Walmart has reported measurable gains in labor efficiency and responsiveness, all while holding management layers flat. This shows how AI agents can act as silent operators, driving cost discipline across vast operations.

Microsoft Copilot: Virtual Manager at Scale

Microsoft’s Copilot is more than a productivity tool—it’s a digital management layer embedded into Outlook, Excel, and Teams. It summarizes meetings, drafts emails, tracks task progress, and auto-syncs calendars. For knowledge workers and project leads, Copilot reduces the need for administrative support and middle-tier coordination—streamlining workflows across large teams without increasing HR overhead.

IBM and ServiceNow: Enterprise Workflow Orchestration

Platforms like IBM Watson Orchestrate and ServiceNow Now Assist empower enterprises to automate HR, legal, and IT management workflows. These agents interpret requests, execute policies, and escalate when needed—replacing layers of mid-level process owners. In some deployments, over 50% of approval-chain decisions are now made by agents. These systems reduce cycle time and enforce compliance with near-zero human latency.

These use cases demonstrate that AI agents are not experimental—they’re already managing workflows, resources, and performance at scale. Firms deploying them early are building leaner, faster, and more responsive operating models—with investor-visible results.

How AI Agents Are Shifting Corporate Margins

From Labor Cost to Software Spend

When companies replace middle managers with AI agents, the immediate shift is from recurring labor expense to predictable software or infrastructure cost. Instead of paying $120,000+ per manager per year, companies spend a fraction on API access, cloud compute, and LLM licensing. This shift creates a fixed-cost digital labor force, improving profit visibility and planning accuracy.

SG&A Compression in Real Time

Middle management costs sit squarely within SG&A (Selling, General & Administrative expenses), which typically consumes 20–40% of a company’s revenue. As AI agents take over reporting, coordination, and supervision tasks, early adopters are already reporting lower SG&A as a percentage of revenue. This kind of efficiency gain doesn’t just improve margins—it signals operational maturity to the market.

Productivity Without Headcount Growth

Perhaps the most powerful impact: output grows while payroll stays flat. AI agents can manage more workflows, monitor more employees, and make more decisions without needing to be “hired.” This allows companies to scale functions like customer service, HR compliance, and project management without adding supervisors. The result is higher revenue per employee—a key investor metric.

The Earnings Effect: Quiet but Compounding

These gains don’t make headlines, but they show up in quarterly earnings. Companies adopting AI agents often report higher EBITDA margins, flatter org structures, and better cash flow, even when revenue growth is modest. For investors, these are early signals of agent-enabled leverage—before full-scale adoption shows up in annual reports.

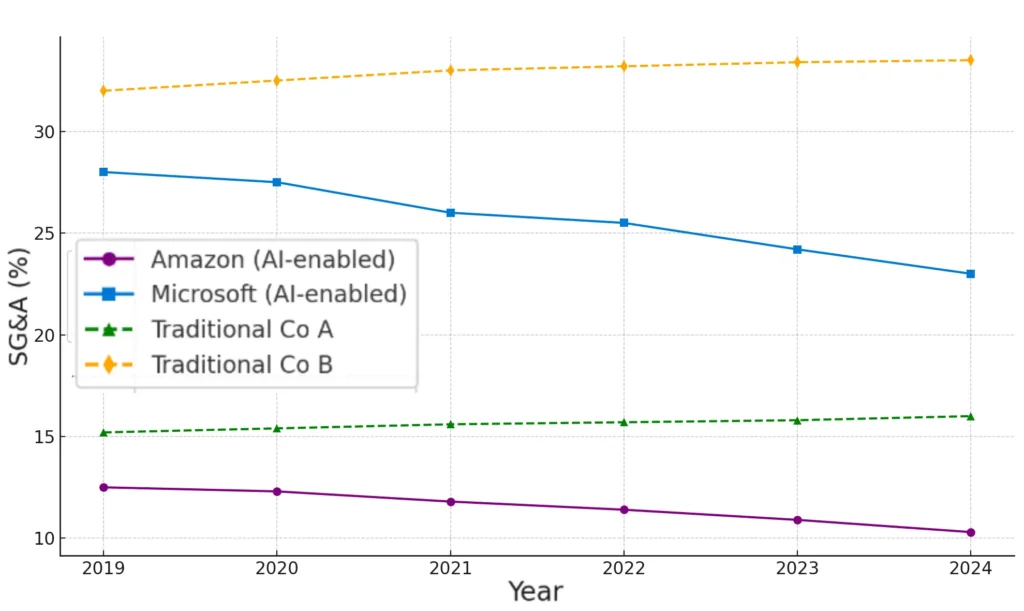

The chart below illustrates how companies deploying AI agents—like Amazon and Microsoft—are already experiencing SG&A compression, in contrast to peers maintaining traditional management-heavy structures.

Public Companies Already Benefiting from AI Agent Efficiency

Amazon: AI in Logistics and Labor Management

Amazon’s deployment of AI agents in warehouse operations has transformed labor allocation, scheduling, and productivity monitoring. These agents autonomously assign tasks, enforce performance thresholds, and resolve conflicts, reducing the need for floor-level supervisors. As a result, Amazon has kept SG&A flat despite expanding fulfillment operations globally—improving its operating income in logistics and services year-over-year.

Microsoft: Productivity as a Platform

Microsoft’s Copilot rollout across Office 365 and Dynamics is doing more than boosting productivity—it’s displacing mid-tier knowledge workers and coordinators. By automating meeting summaries, document generation, and task management, Microsoft is enabling customers to replace layers of manual management with embedded intelligence. Internally, Microsoft has reported operational efficiency improvements, while externally, the company is monetizing AI productivity per seat—without adding personnel.

ServiceNow: Agents for IT and HR Ops

ServiceNow’s AI-native offerings (like Now Assist) are streamlining IT service management, HR case handling, and legal workflow approval chains. These tasks, once managed by coordinators and internal project leads, are now increasingly handled by AI agents. The result is a lower headcount growth rate relative to revenue—driving record-high operating margins in recent quarters.

IBM: Enterprise-Grade Orchestration at Scale

IBM Watson Orchestrate has enabled clients to automate managerial workflows in complex environments—finance, supply chain, and compliance. IBM itself is using these agents internally for process management, while offering them as part of a scalable AI services suite. SG&A improvements have appeared in its consulting and hybrid cloud segments, making IBM a quiet beneficiary of agent-led operational leverage.

Adobe: Creative Ops with AI Oversight

Adobe is integrating AI agents through Firefly and Creative Cloud workflows. While its agents are oriented toward content and design, they increasingly function as production managers—automating reviews, approvals, and asset coordination. Adobe has achieved strong margins and revenue per employee growth without proportional expansion of operational teams.

These companies are not just experimenting—they’re re-architecting how work is managed, replacing middle-layer friction with scalable digital decision-makers. Investors watching SG&A trends, operating margins, and workforce structure disclosures will see the earliest signals of AI agent adoption translating to shareholder value.

Why Middle Management Is the Perfect Target for AI Replacement

Cost-to-Value Mismatch

Middle management roles often come with high salaries, but a significant portion of their work—status reporting, task delegation, compliance checking, and performance monitoring—is rule-based and repeatable. These responsibilities are ripe for automation, especially when AI agents can replicate the function at a fraction of the cost. In economic terms, companies are spending top-tier dollars for mid-tier complexity. AI agents invert this equation—delivering faster, cheaper, and scalable output with consistent quality.

Workflow Complexity, Not Human Complexity

Unlike executive leadership or creative R&D, middle managers deal with structured complexity. Their tasks require juggling calendars, resolving routine bottlenecks, enforcing KPIs, and managing resource allocations—activities that are data-driven and procedural. AI agents thrive in this environment. By integrating with project management tools, internal databases, and communication platforms, agents can execute these workflows in real-time and escalate exceptions only when human intervention is needed.

Scalability Without Bureaucracy

Traditional management scales by adding more layers—more managers, more reports, and more coordination overhead. But every additional layer slows down decision-making and increases SG&A. AI agents enable horizontal scalability: one agent can oversee dozens of workflows, flag deviations, and initiate corrective action without creating new layers of hierarchy. This improves agility and cost-efficiency simultaneously.

A New Layer of Digital Oversight

Replacing middle management doesn’t eliminate oversight—it digitizes it. Companies deploying agents are introducing new roles: AI supervisors, agent orchestrators, and escalation managers. These roles oversee not people, but process logic and autonomous systems. As a result, firms can reallocate human capital toward strategic, creative, or client-facing activities, where human strengths still dominate. This redeployment further amplifies the ROI of replacing repetitive management layers with intelligent software agents.

New Metrics for a New Era: Rethinking Management Efficiency

Why Traditional Ratios Fall Short

In a world where AI agents are replacing human managers, classic efficiency metrics like revenue per employee or headcount growth vs. revenue become increasingly outdated. These metrics assume that human labor is the primary engine of value creation. But when decision-making and task coordination are automated, a new layer of “digital labor” must be accounted for.

AI Leverage Ratio: Measuring Digital Workforce Impact

A forward-looking metric is the AI Leverage Ratio:

Revenue / (Human Employees + Active AI Agents)

This ratio gives a clearer view of how effectively a company scales operations with a hybrid workforce. Firms with a growing number of deployed AI agents—especially those handling managerial tasks—will show rising output per “decision-making unit.”

SG&A Automation Index

Instead of just tracking SG&A as a percent of revenue, investors can now look for SG&A automation signals: declining SG&A costs alongside rising task volume or revenue. This implies not just spending cuts, but agent-driven process efficiency.

Decision Velocity Score

AI agents don’t just reduce costs—they accelerate execution. A valuable metric to track is decision velocity:

Time to close a task, approve a request, or respond to incidents

Firms deploying agents often report significant gains in speed, responsiveness, and cycle-time reduction—hallmarks of a flatter, more digital organization.

Revenue per Agent vs. Revenue per Employee

In companies disclosing agent utilization, a breakout of revenue per AI agent vs. per human employee can offer insight into where true value scaling is coming from. This also helps investors spot companies that are reaping digital leverage, not just automating for optics.

These new metrics will define the next phase of performance benchmarking—rewarding companies that blend human and AI resources with precision and intent.

Sectoral Impact: Which Industries Will Win or Lose?

Big Winners: Scalable, Structured Industries

Industries with large, process-driven operations and high managerial overhead stand to gain the most from AI agents. These include logistics, retail, enterprise SaaS, BPO, and financial services. In these sectors, coordination, compliance, and communication can be digitized at scale. AI agents can oversee onboarding, scheduling, reporting, and customer interactions—enabling firms to grow without proportionally increasing headcount.

At-Risk: Services Relying on Manual Oversight

Sectors such as traditional consulting, legal services, mid-tier HR firms, and legacy IT outsourcers are more vulnerable. Their value models often rely on labor arbitrage, billable hours, and process oversight—all areas where AI agents can now operate efficiently and at lower cost. Unless these firms pivot to offering agent-enabled solutions or proprietary frameworks, they risk margin erosion and client attrition.

Transitional Industries: Healthcare, Education, and Manufacturing

These sectors present complex trade-offs. While healthcare administration and education operations can be partially automated with AI agents (e.g., scheduling, documentation, workflow alerts), direct human interaction remains core. Similarly, manufacturing can benefit from AI in production planning and quality control, but agent deployment depends heavily on sensor integration and physical workflows.

The Rise of “Agent-First” Business Models

Some startups and tech-forward incumbents are redesigning their entire organizational structure around AI agents. In these models, agents are the default managers, and humans are supervisors, creators, or exception handlers. These firms operate with extreme lean overhead and high output per worker—pushing the boundary of what “digital-first” really means.

How Traditional Service Firms Can Pivot and Survive

Shift from Labor to Systems Thinking

Traditional service firms—especially in consulting, HR, legal, and BPO—must stop selling human labor and start delivering scalable systems. Instead of staffing analysts and managers, they should offer clients AI-enabled workflows, digital playbooks, and agent orchestration models. The real opportunity is in becoming transformation partners, not headcount providers.

Build and Monetize Proprietary AI Agents

Firms with deep domain knowledge can encode that expertise into AI agent frameworks. For example, a legal firm could offer a contract-review agent trained on its proprietary risk logic. An HR firm could deploy onboarding agents with built-in compliance logic. These can be monetized as subscription tools or bundled into managed services, turning knowledge into IP.

Reskill Humans as AI Orchestrators

The manager of the future won’t supervise people—they’ll supervise agents. Service firms should retrain consultants, project managers, and analysts to become AI supervisors: professionals who configure, monitor, and improve agent workflows. Skills like prompt engineering, agent behavior tuning, and digital escalation design will become essential.

Rethink the Business Model

Billing by the hour no longer aligns with value in an AI-enabled world. Successful firms will shift to outcome-based pricing: charging by workflow automated, cost reduced, or results delivered. They may also move into SaaS-like recurring revenue through platform access, agent deployment kits, or hybrid advisory + automation retainers.

Firms that pivot early will lead the market. Those that hesitate risk becoming legacy vendors in a post-human-management economy.

Investor Takeaways: Positioning for the Management Automation Era

Look for Early Adopters with Margin Signals

Firms deploying AI agents into management functions often show subtle but powerful shifts: declining SG&A as a percentage of revenue, rising productivity per employee, and faster decision cycles. These signals won’t always be headline news, but they appear in earnings calls, workforce trends, and cost line breakdowns. Investors should prioritize companies showing early operational leverage driven by digital workflows.

Track Agent-Native Platforms and Builders

Software companies that build, embed, or enable AI agents will be key beneficiaries. This includes:

- Builders: OpenAI, Anthropic, Cohere

- Enablers: Microsoft, ServiceNow, Salesforce

- Infrastructure Players: AWS, Azure, Snowflake

These firms will monetize both internally (cost savings) and externally (agent-based product offerings). Exposure to them can offer compounding upside as AI agents become standard enterprise tools.

Monitor the Workforce Shift

Keep an eye on how companies restructure their organizations. Are they reducing mid-level hiring? Reclassifying managerial roles? Launching internal AI agent orchestration teams? These are telltale signs of long-term automation strategy, and early movers are likely to unlock durable cost advantages.

Align with New KPIs

As explored in Section 7, traditional metrics won’t fully capture the impact of AI agent adoption. Investors should consider building frameworks that factor in digital labor productivity, AI leverage ratios, and workflow automation penetration. These adjusted views will reveal underpriced efficiency plays in a rapidly evolving corporate landscape.

This isn’t just about chasing the next AI trend—it’s about recognizing a structural change in how organizations scale, make decisions, and drive margins.

Conclusion: The Agent Dividend Is Real—If You Know Where to Look

The age of AI agents is quietly redrawing the blueprint of corporate leadership. Middle management—once considered untouchable due to its judgment and coordination responsibilities—is now becoming a prime target for automation. Companies that integrate agent-driven operations are not just trimming fat; they’re architecting a new foundation for speed, scale, and margin.

This transformation is more than a technology trend—it’s an economic realignment. Firms leveraging AI agents are achieving operating leverage without labor growth, compressing SG&A, and executing decisions at a velocity unattainable by traditional structures. These changes may not scream from press releases, but they echo in earnings margins, cost ratios, and market positioning.

For investors, the message is clear: follow the workflows, not the hype. Look beyond flashy AI announcements and focus on structural signals—declining administrative overhead, agent disclosures, and flat headcount paired with revenue expansion. This is where the next wave of alpha lies. The “agent dividend” will accrue not to those who speculate on AI—it will reward those who understand where intelligence becomes infrastructure.

📚 References

- McKinsey & Company (2023) – The Economic Potential of Generative AI

https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier - Gartner (2024) – Top Strategic Technology Trends: AI-Augmented Work

https://www.gartner.com/en/articles/top-strategic-technology-trends - Microsoft (2024) – Microsoft Copilot and the Future of Work

https://www.microsoft.com/en-us/microsoft-365/blog - Amazon (2023) – Annual Report: AI in Warehouse Operations

https://www.aboutamazon.com/news/company-news/2023-annual-report - Walmart (2023) – Earnings Call Transcript Highlighting AI Scheduling Tools

https://corporate.walmart.com/news/earnings - ServiceNow (2024) – Now Assist and Intelligent Workflow Automation

https://www.servicenow.com/products/now-assist.html - IBM (2024) – Watson Orchestrate Product Overview

https://www.ibm.com/products/watson-orchestrate - Accenture (2024) – AI in the C-Suite: Transforming Management Models

https://www.accenture.com/us-en/insights/artificial-intelligence/generative-ai - PwC (2023) – AI and the Future of Work: Sizing the Prize

https://www.pwc.com/gx/en/issues/analytics/assets/pwc-ai-analysis-sizing-the-prize-report.pdf - Harvard Business Review (2023) – How AI Will Reshape Middle Management

https://hbr.org/2023/10/ai-wont-replace-managers-but-it-will-transform-their-roles

🔑Keywords:

- AI agents in business

- middle management automation

- AI replacing managers

- agentic AI economics

- AI in enterprise operations

- SG&A automation trends

- digital labor transformation

- AI investment signals

- enterprise AI adoption

- AI-driven margin expansion

- workforce automation strategy

- autonomous enterprise software

- AI-powered corporate structure

- management automation ROI

- AI-enabled business models

⚠️ Investment Disclaimer

The information presented in this portfolio allocation is for informational and educational purposes only and does not constitute financial, investment, or legal advice. It is not intended as a recommendation to buy, sell, or hold any securities or investment products. The allocation model reflects general market trends and publicly available research at the time of writing, and may not be suitable for all investors. Please consult with a licensed financial advisor or professional before making any investment decisions.